FHA, VA, or Conventional Loans in 2026: Which Mortgage is Right for You?

Understanding Your Mortgage Options for 2026

Navigating the housing market in 2026 requires a clear understanding of your financing options. Whether you are a first-time buyer or looking to refinance for better rates, selecting the right mortgage product is the most critical step in your homeownership journey.

At United Mortgage Corporation of America, Michael Harris and our experienced team of Mortgage Advisors are dedicated to helping you compare and choose the perfect home purchase loan. Let us break down the primary loan types available this year to help you make an informed financial decision.

- Conventional Loans: Ideal for buyers with strong credit.

- FHA Loans: A great entry point for first-time buyers.

- VA Loans: Exclusive benefits for our honorable veterans.

Comparing FHA, VA, and Conventional Home Loans

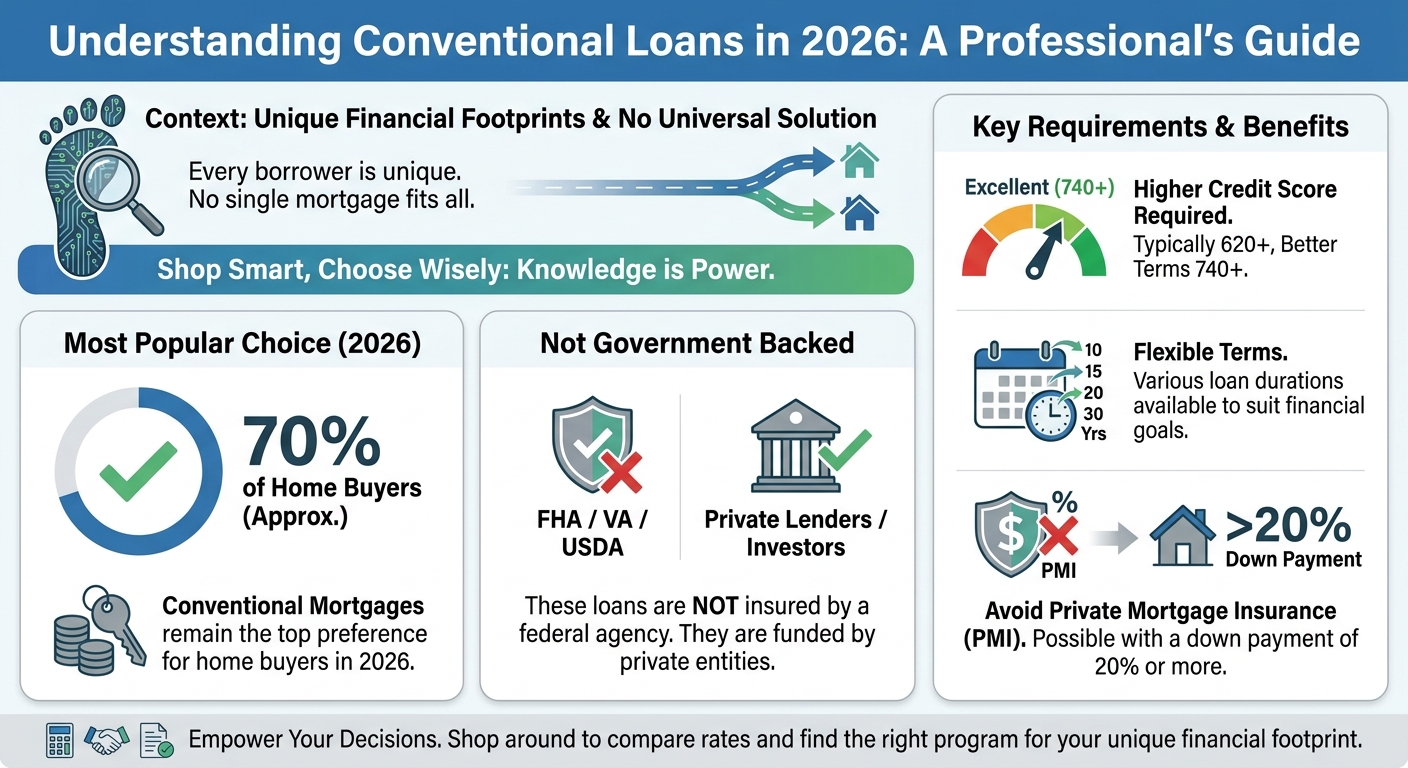

Every borrower has a unique financial footprint, which means there is no universal mortgage solution. When you shop around for the best rate, understanding the nuances of each program gives you the power to choose wisely.

Conventional Loans

Conventional mortgages remain the most popular choice for home buyers in 2026. These loans are not backed by a government agency. They typically require a higher credit score but offer flexible terms and the ability to avoid private mortgage insurance with a twenty percent down payment.

FHA Loans

Backed by the Federal Housing Administration, FHA loans are designed to make homeownership more accessible. They offer lower minimum credit score requirements and down payments as low as 3.5 percent. If you are looking to secure your home purchase loan with less cash upfront, an FHA loan might be your best path forward.

VA Loans

Reserved for active-duty military members, veterans, and eligible surviving spouses, VA loans offer incredible terms. Backed by the Department of Veterans Affairs, these loans require zero down payment and no private mortgage insurance. It is one of the most powerful lending tools available today.

Ready to see where you stand? Get your FREE Pre-Approval Letter today to evaluate your property and purchasing power.

| Loan Type | Minimum Down Payment | Minimum Credit Score (Typical) | Mortgage Insurance Required? |

|---|---|---|---|

| Conventional | 3% to 20% | 620 | Yes (if under 20% down) |

| FHA | 3.5% | 580 | Yes (Upfront and Annual) |

| VA | 0% | No official minimum (often 580+) | No (Funding fee applies) |

How to Choose the Best Mortgage for Your Future

Choosing between an FHA, VA, or Conventional loan depends entirely on your current savings, credit history, and long-term financial goals. Taking advantage of today’s competitive rates requires working with a trusted local professional who can guide you efficiently and confidently.

At United Mortgage Corporation of America, Michael Harris is ready to help you analyze your options. Whether you want to accomplish a strategic refinance, consolidate debt, or secure your first home, our 100% online loan application makes the process seamless. We can often get your loan funded in less than 30 days.

Compliance Notice: All loans are subject to credit approval. Interest rates and loan programs are subject to change without notice. United Mortgage Corporation of America is an Equal Housing Opportunity lender.

Q1: What is the main difference between FHA and Conventional loans?

FHA loans are government-backed and have lower credit and down payment requirements, whereas Conventional loans are not government-insured and typically require stronger credit profiles.

Q2: Can I refinance an FHA loan into a Conventional loan in 2026?

Yes, many homeowners refinance from FHA to Conventional loans to eliminate mortgage insurance once they build enough equity in their property.

Q3: Are VA loans only for first-time home buyers?

No, eligible veterans and active military personnel can use their VA loan benefits multiple times for primary residences, provided they have remaining entitlement.

Q4: How long does the mortgage pre-approval process take?

With our quick and easy tools at United Mortgage Corporation of America, you can get customized rate comparisons and pre-approval letters quickly, often within a single day.

Q5: Does a larger down payment get me a better mortgage rate?

Generally, putting more money down reduces the lender’s risk, which can help you secure a lower interest rate and avoid costly private mortgage insurance.

Get Your Mortgage Rate Quote in Just 30 Seconds with Michael Harris!

United Mortgage Corporation of America NMLS #3189 | CA: Dept. of Real Estate Officer #01870497 | CO: Regulated by the Division of Real Estate #100524628 | MT: Mortgage Broker No #3189 | TX: 4663 Farringdon Ln. | WA: Consumer Loan Company License CL-3189. MLO NMLS #233410 | CA: Brokers License #00991234 Equal Housing Lender.